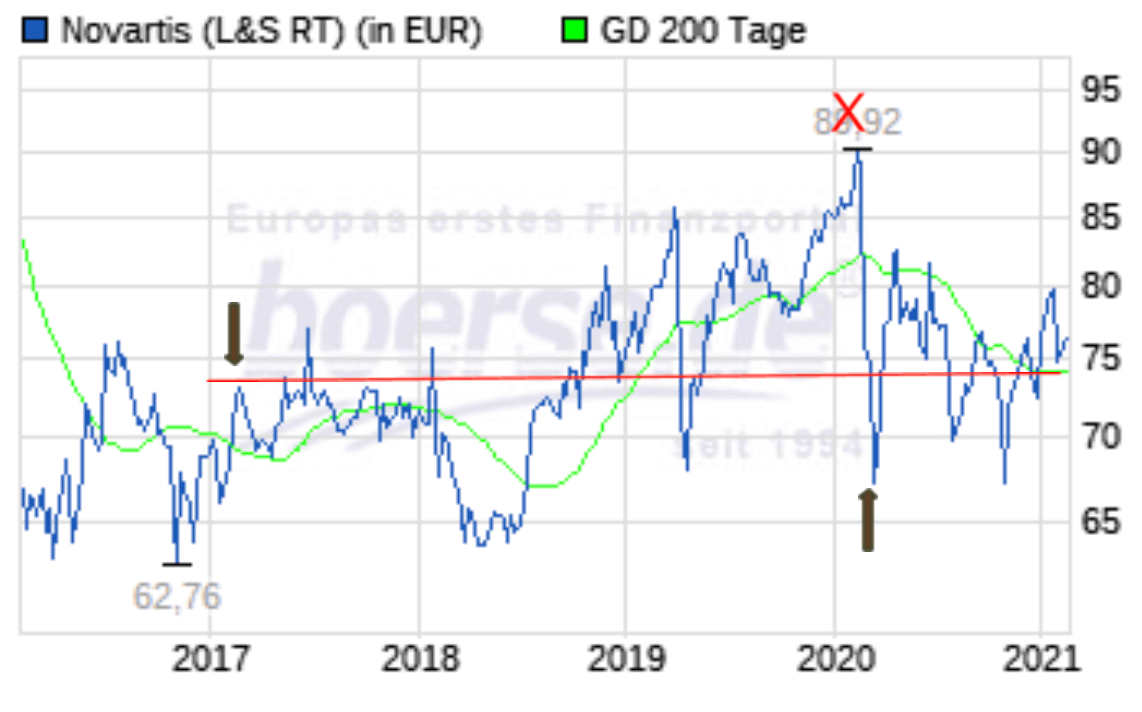

Novartis AG is a company under Swiss law; the employment relationship of cross-border commuters is also determined by Swiss law. Consequently, the civil law consequences of the employment relationship are also assessed according to the provisions of the Swiss Civil Code. Whether and when a transfer of ownership has taken place within the framework of the various employee participation models is therefore only a secondary assessment by the BFH. Judgments in this regard are not yet known. Novartis' programs do not provide for an obligation to purchase the shares. Assuming there is an inflow, then the inflow cannot be taxed at the market value. The fact that Novartis shares are highly volatile can be seen in the following graphic:

An inflow within the meaning of § 11 According to the established case law of the Federal Finance Court, EStG is only accepted when economic control is obtained. This is not the case if the employee cannot or cannot yet dispose of the shares. Anyway, let's pretend that there was "inflow" to the stock. What value does it have then? The stock represents the market value when all rights that are transferred with ownership of the share are comparable to the rights when buying a share. Stocks are investments in companies. They are worth as much as can be earned from future withdrawable income, provided they can be used at any time of the day or night. To ensure this, the stock exchanges exist.

From the time of the tax inflow, more recently from July 1st also when changing employers, at the latest from the exercise of the option right, the increase in value is no longer taxed as employment income, but rather as capital income upon sale. This was recently confirmed by the BFH in its judgment of October 4.10.2016, 43 - IX R15/XNUMX.

The transfer of shares represents a benefit in kind that is to be valued at the time when economic control is created. Let's take the chart shown above. If he bought the share at the beginning of 2017 at the stock market price of 74, a shareholder would have the opportunity to sell it at any time, including in spring 2020 at the stock market price of around 90. No shareholder would allow this right to be taken away. If so, he wants something in return. Exactly what he wants in return is the amount by which the benefit in kind deviates from the market value. An employee who was allocated the shares at the same time as part of a program cannot take advantage of the opportunity and may have to wait until the three years are over and the share prices have crashed due to whatever. He would be obliged to tax income in 2017 that he never received and never will receive. He couldn't even offset the exchange rate losses against his employment income for tax purposes. This would violate the principle of taxation based on ability to pay.

Ergo:

The taxation of the acquisition of an employee shareholding at the time of allocation and in terms of the amount at the stock market price violates the principle of taxation based on performance in terms of time and amount. It therefore remains to be seen whether the new law, which will apply from July 1, 2021, will withstand judicial review.